What can retail financial services firms learn from the IDD experience?

Our own IDD experience tells us three things:

- Regulatory obligations aren’t inevitably at odds with commercial strategy

- Iterative user-centred design helps locate the sweet spot where both are met

- The second best time to adopt it is now – surprising improvements can be delivered more quickly than you might think

Back in early 2018, many general insurers and their brokers had optimised their sales funnels by adopting e-commerce techniques proven to make products easier to buy. Purchase journeys played successfully to our biases towards default options, loss aversion, and our desire to make grudge purchases as painless as possible. Meanwhile, price comparison sites had made it easier to see which products were cheapest.

Ease and low cost sound like benefits for consumers, but the FCA saw a downside – too many people were happily buying the wrong thing. The result?

- Mismatched expectations caused by poor understanding

- People paying for features they didn’t need or couldn’t use

- Poor consumer outcomes

- Eroding trust in the industry

Is there an echo in here?

As the IDD deadline approached, the floor began to wobble and tension between compliance and commercial teams rose in firms across the sector. This latent tension hinges on the belief that it’s a zero-sum game: if you win then we lose, if you increase compliance then we’ll see less profit.

The work we did with some firms made them rethink that belief.

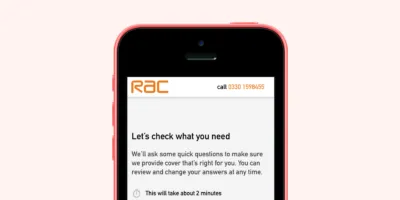

The RAC was one of those that approached us to help ride out the tremor. There wasn’t much time. Our brief was to quickly design a technically viable, evidently compliant purchase journey, and to minimise the inevitable commercial damage.

Our tailored user-centred design approach proved a good fit.

We designed a journey that demonstrably improved consumer understanding and delivered an +8% increase in revenue. Better for customers and for the business.